Wage garnishment, also sometimes referred to as a wage attachment, is an order that requires your employer to withhold a certain amount of money from your paycheck. Instead of getting this money, it is sent to one of your creditors. Except for rare cases, this requires that the creditor first get a money judgment from the courts.

Getting control of your own wages again can be a frustrating process, one that often isn’t achieved until the full amount has been paid off. However, there are rare situations that can make it easier to get a wage garnishment stopped. Thankfully, there is a limit to how much can be taken from your paycheck.

We’re going to first look at the limits that North Carolina has placed on wage garnishment in order to ensure that citizens aren’t made to suffer recklessly at the hands of such garnishment. After that, we’ll look at ways that can be used to help protect yourself from wage garnishment. Finally, we’ll close out by looking at a way to stop wage garnishment and the value there is to be gained by working with a professional to solve the issue.

Are There Limits on Wage Garnishment in North Carolina?

North Carolina is actually one of the better states in terms of wage garnishment. In fact, if they had it their way, creditors would not be able to garnish wages even if they had a money judgment. However, out-of-state creditors are able to garnish wages from those living in North Carolina. Also, certain debts owed to the federal government or to a federal agency can be garnished in North Carolina.

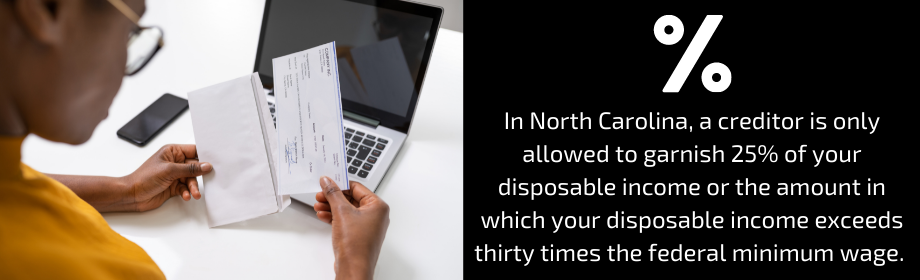

In North Carolina, a creditor is only allowed to garnish 25% of your disposable income or the amount in which your disposable income exceeds thirty times the federal minimum wage. Thankfully, they are only allowed to garnish the lower of these two rather than the higher. A creditor can, however, rely on alternative means of collecting the debt owed to them and so this limit on wage garnishment does not equate to freedom from the hassles of creditors.

In addition to the limited amount that creditors can garnish, creditors are only able to garnish wages for specific kinds of debts:

- Ambulance bills (depending on the county)

- Alimony

- Court-ordered arrears

- Court-ordered child support

- Income taxes left unpaid.

- Student loans that have defaulted

- Unemployment benefit overpays

- Debts owed to a creditor in a state that allows wage garnishment

Keep in mind that not all creditors will require a court judgment. If you are found to be owing child support, taxes, or federal student loans then these could be garnished without a judgment. There’s a lot more that goes into how these specific debts are handled but that’s another story that we can get into later if you’re looking to learn more.

How Do You Protect Yourself From Wage Garnishment?

Obviously, the best way to protect yourself from wage garnishment is to avoid it in the first place. Unfortunately, that’s easier said than done. However, if you can work out an alternative payment solution with your creditor, this may allow you to avoid wage garnishment and make life a little smoother.

Some people will suggest getting paid under the table or in cash. While this can help you to keep more money on hand, it’s also going to open you up to additional legal problems that could make your situation far worse than it already is. It’s always better to work within the legal system rather than against it because the punishments will only mean more fines and payments to be made.

One thing that can protect you against wage garnishment is to act quickly when you get a notice for a wage garnishment order. By filing an exemption claim, you may just be able to exempt some of your wages from the wage garnishment order. Raising an objection in this manner is done by several different procedures depending on what type of debt is being collected. It gets complicated rather quickly so you may want to consult with an attorney about the specifics of your wages and debts to see what kind of objections could be raised.

Can You Put a Stop to Wage Garnishment?-

There aren’t a lot of options for stopping wage garnishment once it gets going. The most common and simplest way to put an end to wage garnishment is to pay off the debt that you owe. This could be done by following the order and waiting for the payments taken from your wages to pay it off. Alternatively, if the creditor allows you to then you could make additional payments to get rid of the debt quicker and in doing so end the wage garnishment.

It’s worth noting that one fear people have when they get a wage garnishment order is that their employer is going to fire them. After all, a wage garnishment order adds more work and hassle onto your employer’s shoulders. North Carolina follows federal law which offers protections to employees. If you have a wage garnishment order then your employer is prohibited from firing you. However, if you have more than one wage garnishment order then you could be fired.

Losing your job would mean losing your ability to make a lot of payments in your life and this could lead to bankruptcy. Bankruptcy may be necessary due to the debts you’ve acquired regardless of getting fired. In a neat little twist, bankruptcy is one way that you could potentially end a wage garnishment order without fully paying off the debt. It depends on whether or not the debt causing the garnishment of your wages is eliminated in bankruptcy or not through the bankruptcy discharge.

Can An Attorney Help Me Prevent Wage Garnishment?

If you speak to an attorney early enough, they may be able to help you protect some of your wages from a garnishment order.

That said, if you are considering bankruptcy as a way of ending a wage garnishment order and clearing your debts then you absolutely need to work with an attorney because there’s just too much that could go wrong if you don’t have professional support.