If you have worked hard, but you are nevertheless struggling with your finances, the one thing you do not need is a lawsuit from a creditor. That lawsuit’s consequences could be lasting and serious. If you’re sued by a creditor, contact a compassionate attorney for financial defense at once.

In 2022, consumers in North Carolina owed $33.8 billion in credit card debt, and North Carolina households averaged $7,752 in credit card debt. With statistics like these, it is no surprise that debt collection lawsuits are common – and are increasing – in this state.

What are your rights if you are sued by a creditor in North Carolina? What steps will you need to take? When should you contact a debt defense lawyer? Keep reading this brief discussion of creditor lawsuits and your rights, and you will find the answers to these questions.

What is a Default Judgment?

If you are targeted by a creditor lawsuit, you should be represented by a debt defense lawyer who will either have your case dismissed or negotiate a settlement or provide other options that you can live with. You need an outcome that will not take all of your resources and destroy your future.

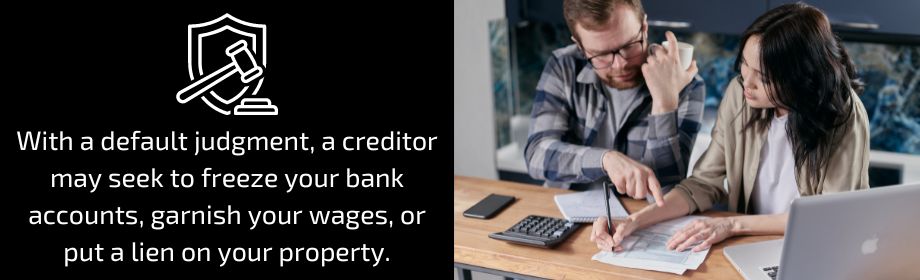

If you ignore the lawsuit and do nothing, a court may award the creditor a “default” judgment, meaning that the lawsuit automatically prevails. With a default judgment, a creditor may seek to freeze your bank accounts, garnish your wages, or put a lien on your property.

If a default judgment is entered against you, the creditor can file legal papers to have the sheriff in the county where you reside garnish your bank accounts or seize other assets.

Here’s a better option: Ask a North Carolina debt defense attorney to review your debt case and to develop an effective defense strategy for you. Your attorney will explain your legal rights and will seek to settle the lawsuit or to have it entirely dismissed.

Do Creditor Lawsuits Always Require Trials?

Creditor lawsuits rarely go to trial. In fact, approximately 90 percent of creditor lawsuits result in default judgments when defendants don’t show up in court. And about 8 percent of these lawsuits end with the defendant agreeing to a payment schedule for the total amount of the debt.

However, over time, many of these defendants cannot afford a creditor’s terms and conditions, and they later end up back in the courtroom. Defendants are represented by debt defense attorneys in only about 2 percent of these cases.

However, the 2 percent of defendants who are represented by debt defense attorneys generally do better in these cases than the other 98 percent. In cases where defendants are represented by debt defense lawyers, a lawsuit is usually either dismissed or settled for a reduced amount.

Your lawyer will also determine if a creditor or a creditor’s attorney violated the federal Fair Credit Reporting Act, the federal Fair Debt Collection Practices Act, the North Carolina Deceptive Trade Practices Act, or any of the other statutes that protect your consumer rights.

What is the Statute of Limitations for Creditors to File Lawsuits?

In North Carolina, creditors usually have three years from the last activity on your account to file a debt lawsuit against you. However, whenever you make a payment on your debt, that payment resets the statute of limitations “clock” and gives the creditor three more years to take legal action.

A creditor may attempt to persuade you to make a small payment, but if it has been three years or more since you have made a payment, speak first to a North Carolina debt defense lawyer. Do not let a debt collector trick you into starting the statute of limitations again.

However, after the statute of limitations expires, the original creditor may continue to pursue you for payment. You may be sued because you still owe the debt. However, you may raise the affirmative defense of the statute of limitations to avoid the debt and have the lawsuit dismissed. After three years of inactivity on your account, a creditor can call you or send letters and may threaten you with a lawsuit. However, the threat may be a violation of the debt collection practices laws.

Is Your Debt Owned by a Debt Purchasing Company?

What is the difference between a debt buyer and a debt collector? A debt collector is usually hired by the original creditor and acts on behalf of that creditor, so a debt collector may legally continue to pursue you about your debt, or collect it, after the statute of limitations has expired.

While original creditors and their hired debt collectors may collect debts after the statute of limitations expires, a debt buyer cannot. If you are being pursued about an old debt by a debt buying company, it means that your debt was sold to the debt buyer by the original creditor.

Debt purchasing companies typically purchase debts at highly discounted rates, and they are barred from collecting a debt in North Carolina after three years from the last activity on your account.

However, if you are sued in North Carolina for a debt by a debt purchasing company before the three-year statute of limitations has expired, take your case at once to a debt defense attorney. If you are sued you should contact a debt defense attorney to determine what defenses you may have including the statute of limitations defense.

What Are the Debt Collection Rules?

Under federal and state consumer protection laws, debt collectors may not:

- use profane, obscene, or abusive language

- call you so often that it constitutes harassment

- call you at odd hours, or at work if they know your employer prohibits personal calls

- threaten to use force or violence

- make false accusations

- threaten to take legal action that they cannot take

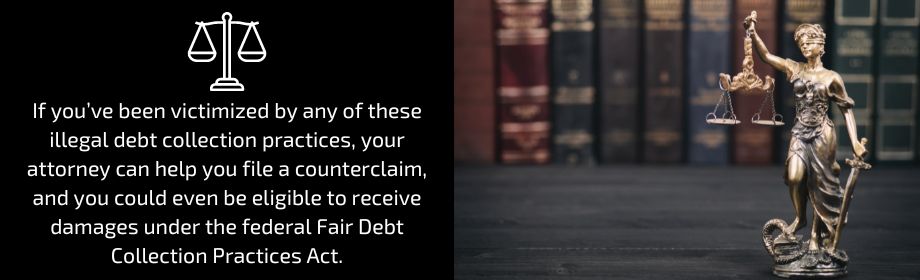

If you’ve been victimized by any of these illegal debt collection practices, your attorney can help you file a counterclaim, and you could even be eligible to receive damages under the federal Fair Debt Collection Practices Act.

What Else Should North Carolina Consumers Know?

If you have taken out a loan or extensively used a credit card, and if you have trouble paying it off, the consequences can be serious. A debt lawsuit is sometimes only the beginning. You could face the repossession of your vehicles or even a foreclosure on your home.

If your debts are overwhelming you, your first step is arranging to speak with a good debt defense lawyer. Bankruptcy is one option, but bankruptcy isn’t right for everyone.

A bankruptcy and debt defense lawyer can explain your options for resolving your debts and recommend the option that will work best for you. If you are sued by a creditor, or if you simply can’t pay your debts, schedule a meeting with a debt attorney at once, and get the help you need.