What Are North Carolina’s Debt Defense Laws?

If you work hard and struggle with your finances, the last thing you need is to be harassed or sued by a debt collector. If you’re being harassed by a debt collector or sued regarding a debt, contacting a North Carolina debt defense attorney is the first step you should take.

What are the state and federal laws that protect consumers from abusive debt collection practices? What are your rights and options if you’re being harassed – or sued – because of a debt? How will a North Carolina debt defense lawyer help you and work on your behalf?

Keep reading for the answers to these questions. What follows is a short discussion of the laws that protect North Carolina consumers from debt collection abuse, and you will learn what steps to take, now or in the future, if your consumer rights are violated in this state.

What Laws Protect You From Abusive Debt Collectors?

A number of state and federal laws regulate debt collection practices and set forth your rights as a consumer. The Fair Debt Collection Practices Act (FDCPA) is a federal statute that defines your rights as a consumer, and it makes intrusive and abusive debt collection practices illegal.

The FDCPA applies exclusively to debt collectors, defined as those who collect debts on behalf of other parties. Original creditors are not regulated by the Fair Debt Collection Practices Act except when they collect debts by using a different name.

At the state level, the North Carolina Collection Agency Act and the North Carolina Debt Collection Act Also protect consumers in this state by regulating debt collection practices and by allowing consumers to recover damages from debt collectors who violate their consumer rights.

What Do North Carolina’s Consumer Protection Laws Provide?

The North Carolina Debt Collection Act (NCDCA) is comparable to the FDCPA, but it offers even more protection to North Carolina consumers. While the FDCPA doesn’t apply to original creditors, for example, the NCDCA applies to anyone collecting a debt from a consumer.

Unlike the NCDCA but similar to the FDCPA, the North Carolina Collection Agency Act regulates only debt buyers and collection agencies. These North Carolina laws allow consumers whose rights are violated to sue for actual damages, statutory damages (at $500 to $4,000 per violation), plus reasonable lawyer’s fees.

A collection agency must obtain a permit to operate in this state, and non-resident collectors are required to post a bond of $10,000. In all correspondence, collection agencies must identify themselves, and an agency must include its true name, address, and permit number.

What Else is Required of Collection Agencies in North Carolina?

Collection agencies must keep full, accurate records of all business conducted in North Carolina. Copies of receipts issued to consumers must be kept in a collection agency’s offices for at least three years.

Any person, corporation, association, or firm conducting debt collections or operating a collection agency without a permit in North Carolina may be charged with a criminal violation – a felony.

A North Carolina mortgage bank does not require a collection agency permit to collect on defaulted loans or on loans that it has purchased. Instead, mortgage banking companies that do business in this state must be licensed by the North Carolina Commissioner of Banks.

How Are Debt Collectors Regulated?

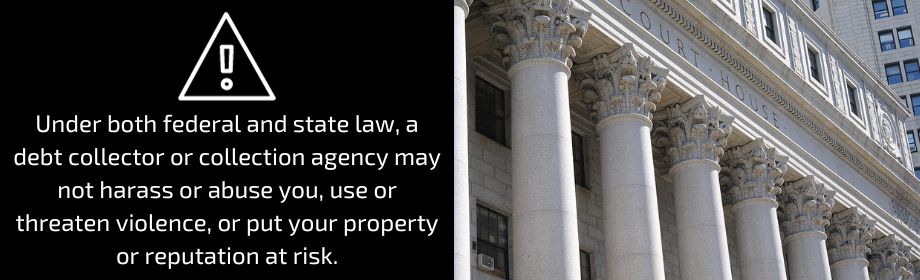

Under both federal and state law, a debt collector or collection agency may not harass or abuse you, use or threaten violence, or put your property or reputation at risk.

Additionally, a collection agency or debt collector may not:

- call you repeatedly

- call you before 8:00 a.m. or after 9:00 p.m. without your consent

- use threats or obscene or abusive language

- try to collect more than you owe or misrepresent the amount of your debt

Additionally, debt collectors may not contact you at your job after being told that you cannot take personal calls at work.

Do You Need an Attorney’s Help?

If you are getting threatening letters or harassing phone calls from a debt collector, you’re like thousands of others in North Carolina. What are your options for ending the harassment? Reach out immediately for help by contacting a North Carolina debt defense attorney.

If a debt collector or a collection agency has violated your rights, you may bring a harassment lawsuit against the agency or collector. Consumers often prevail and are awarded damages in these cases.

Are You Being Sued for a Debt?

If you’re hit with a debt collection lawsuit, you may have a genuine defense. If the debt is someone else’s, or if the creditor violated your rights, a North Carolina court may dismiss the case or find in your favor.

In most lawsuits arising from debts, however, the defendant in fact owes the debt but can’t pay it. If this is your situation, you must respond quickly to the lawsuit. A North Carolina debt defense lawyer may be able to negotiate a settlement.

How a debt lawsuit is resolved in North Carolina will depend on a number of factors, but most of these cases are either dismissed or settled for less than the original debt amount.

However, if you ignore a debt collection lawsuit, the court may award a default judgment to the debt collector, who may then freeze your bank accounts, seek to sell your assets through a Sheriff’s sale, or even place a lien on your home. But how can you find a lawyer who will defend you aggressively and effectively?

Why Should You Choose Gillespie & Murphy?

There’s no need to search extensively for a debt defense attorney. If you’re being harassed or sued by a debt collector, the award-winning legal team at Gillespie & Murphy will explain your options and rights and find the solution that works best for you.

Gillespie & Murphy provides the sound legal advice that helps consumers in North Carolina make the right choices. Our offices are located in Greenville, Jacksonville, Wilmington, and New Bern.

Gillespie & Murphy also helps consumers who are facing vehicle repossession or foreclosure on a home, and if bankruptcy is the right option for you, we will guide you through the bankruptcy process.

If your consumer rights are violated, if you’re sued for a debt, or if you need a solution to your debt problem, call Gillespie & Murphy promptly at 252-659-5045 to schedule a consultation with no cost and no obligation. If debt is the problem, Gillespie & Murphy will find the solution.